Employers in California to Pay Higher FUTA Tax Rates Retroactively

Employers in California, Connecticut, Illinois, New York, and the U.S. Virgin Islands will pay higher Federal Unemployment Act (FUTA) taxes in January 2023 for wages paid in 2022 due to unpaid federal loans. The Department of Labor & IRS recently announced that the Credit for FUTA taxes will be reduced for employers in these states. This results in an adjusted higher net tax rate. This increase will be based on FUTA taxable wages paid in the affected jurisdictions during 2022. This adjusted higher net rate must be calculated retroactively for 2022 and paid in January of 2023.

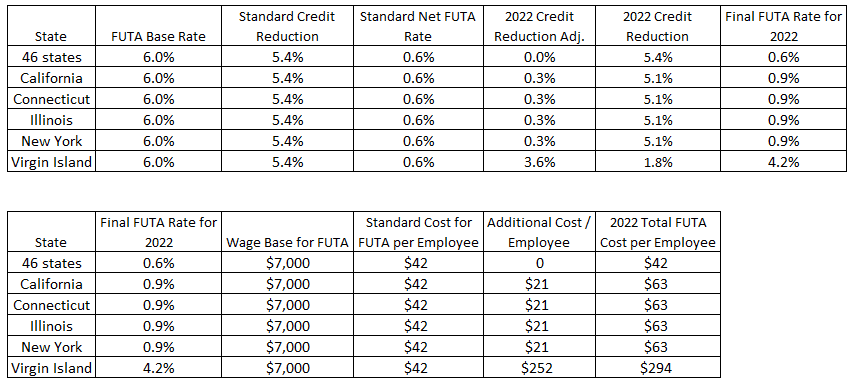

California Employers will pay an additional 0.3% on FUTA taxable wages (first $7,000 of taxable wages times 0.3%, or up to $21 per employee) when the 2022 Form 940 is filed.

According to IRS regulations, any increased FUTA tax liability due to a credit reduction is considered incurred in the fourth quarter (for that calendar year) and is due by January 31 of the following year.

The state of California has an outstanding loan balance on unemployment loans. The California Unemployment fund borrowed funds from the Federal unemployment trust account to pay for Unemployment claims during the pandemic and has not repaid those funds. The states have until November to repay the outstanding federal loans to avoid credit reductions for their state.

The FUTA tax “credit” employers normally receive is being reduced as a result of the state of California’s outstanding loan balances with the Federal Unemployment Trust Fund. California is one of five jurisdictions that still had an outstanding loan balance in November 2022 (for the years 2020 through 2022) that resulted from high unemployment primarily due to COVID-19. The state of California did not fully repay the federal loan by the deadline of November 10th, and the standard “credit” is reduced. Thus, employers in the state will be required to pay a higher FUTA rate retroactively to January 1 of 2022. California’s unemployment loan balance as of December 6th is at $18,309,479,411.59.

Beginning January 1 of every calendar year, FUTA is calculated on the first $7,000 of wages for every eligible employee. The base FUTA tax rate is 6.0%, with a standard credit of 5.4%. This equals a standard net rate of 0.6%. (6.0% – 5.4% = 0.6%)

As a result of the credit reduction status, the 5.4% credit is being reduced by 0.3%, to 5.1% resulting in adjusted net FUTA tax rate of 0.9% Credit Reduction of 0.3% adjusts the net credit to 5.1% (5.4% – 0.3% = 5.1%)

Below are charts of states and jurisdictions with their associated credit reductions. The additional amounts below are the maximum amount per employee for 2022.

Adjusted Net Rate: 6.0% – 5.1% = 0.9%

(An increase of 0.3% – up to $21.00 for each employee in CA)

*FUTA is calculated on the first $7,000 of wages per year per employee.

Example:

XYZ Sample Company has 100 employees in California in 2022. As such, XYZ Sample Company’s FUTA tax due on each employee’s wages paid in 2022 would be $42 ($7,000 x 0.6%), or a total of $4,200 ($42 x 100). Because California is subject to the credit reduction, the FUTA tax owed per employee is $63 ($7,000 x 0.9%). This is an increase over the normal FUTA payment of $42 for each employee who earns $7,000 or more annually. The 2022 FUTA tax for an employer in California with 100 employees will be $6,300 ($63 X 100) rather than $4,200, which is an increase of $2,100.

A brief video that explains the FUTA credit reduction is available on the IRS website. You can view it here: https://www.tax.gov/SmallBusinessTaxpayer/Employers/FUTACreditReduction