Federal Unemployment Tax Credits Reduced for California Employers Retroactively for 2025

California, along with the U.S. Virgin Islands, is once again facing a reduction in Federal Unemployment Tax Act (FUTA) credit for 2025. This means employers in California will pay higher FUTA taxes retroactively on wages paid in 2025 due to the state’s outstanding federal unemployment insurance loans.

The FUTA Tax Credit Reductions effectively increase the tax liabilities by 1.2% on the first $7,000 of wages for each employee in 2025 for California employers. Employers in the U.S. Virgin Islands face a 4.5% FUTA credit reduction. The additional amounts are due in January 2026 with the 2025 fourth-quarter federal unemployment tax payment. See chart below.

What Is the Federal Unemployment Tax Act (FUTA)?

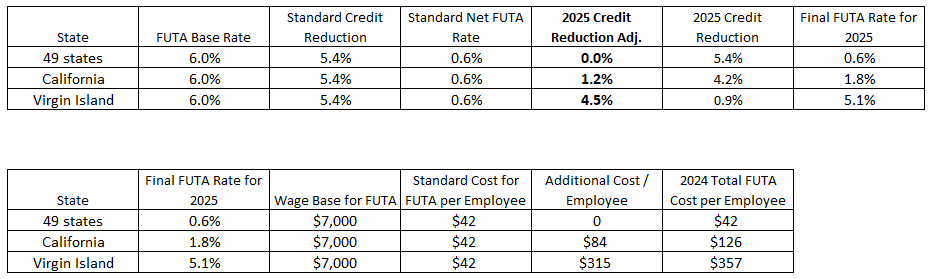

The Federal Unemployment Tax Act (FUTA), enacted in 1939, established a federal payroll tax that funds state workforce agencies and supports unemployment benefits for workers nationwide. The base federal FUTA tax rate is 6.0% on the first $7,000 of each employee’s wages, which is paid entirely by employers.

In most states, employers receive a credit of 5.4%, reducing the net FUTA rate to 0.6%. However, when a state has outstanding federal unemployment insurance loans (also known as Title XII advances) and fails to repay them by November 10 of a given year, employers in that state lose part of that credit.

When this occurs, the FUTA tax rate increases proportionally by the amount of the credit reduction. The increased tax applies retroactively for the year and is payable with the Form 940 filing due January 31 of the following year.

Understanding California’s 2025 FUTA Credit Reduction

According to the U.S. Department of Labor, several states initially faced a potential FUTA credit reduction in 2025. However, the state of New York repaid their outstanding federal unemployment loan balance before November 10, 2025, avoiding a credit reduction.

California had an outstanding loan balance on each January 1 from 2021 through 2025 and did not repay all advances before the November 10, 2025 deadline. The state applied for a waiver of the fifth-year Benefit Cost Rate (BCR) add-on, which was approved by the U.S. Department of Labor. The “BCR add-on” waiver avoids an additional credit reduction for 2025. Therefore, employers in California are subject only to a 1.2% FUTA credit reduction for 2025.

The U.S. Virgin Islands also had outstanding advances on each January 1 from 2010 through 2025 and received approval for the same BCR waiver, leaving employers in the Virgin Islands with a 4.5% FUTA credit reduction.

How the FUTA Tax Rate Is Calculated

Each calendar year, the FUTA tax applies to the first $7,000 of each employee’s wages. The standard FUTA credit is 5.4%, which, when subtracted from the 6.0% base rate, results in a net rate of 0.6%.

For states with outstanding advances, a credit reduction is applied. This credit reduction increases by 0.3% for each consecutive year the state carries an unpaid balance.

For 2025:

- California’s FUTA credit reduction is 1.2%, resulting in a final FUTA rate of 1.8%.

- Virgin Islands employers face a 4.5% credit reduction, resulting in a final FUTA rate of 5.1%.

What California’s 2025 FUTA Credit Reduction Means for Employers

Employers in California are required to pay the adjusted FUTA rate of 1.8% for 2025 retroactively when filing Form 940 in January 2026.

For example:

An employer with 50 employees in California would normally owe $42 per employee (0.6% FUTA tax on the first $7,000 in wages), or $2,100 total. With the 1.2% FUTA credit reduction, the cost increases to $126 per employee, or $6,300 total for the business.

The IRS has provided specific guidance for employers in credit reduction states on how to calculate and report these changes on Form 940.

California’s Outstanding Federal Loan Balance

As of the end of 2025, California continues to maintain an outstanding Title XII federal unemployment insurance loan balance, having held unpaid advances since 2021. Although the state qualified for a waiver of the fifth-year BCR add-on, repayment of the principal loan remains pending.

If California does not repay its balance by November 10, 2026, employers can expect an additional credit reduction for the 2026 tax year. Employers are encouraged to plan accordingly for potential future increases in the FUTA rate.

This information is provided as a courtesy and should not be considered legal or tax advice for business owners or payroll professionals. For specific guidance on how California’s FUTA credit reduction may affect your business, please consult a qualified CPA, tax attorney, or tax advisor.

For more information, please visit the United States Department of Labor FUTA page.