1. Speak with a wage and hour specialist.

You aren’t a number to us. We work with you to build a long-term relationship..

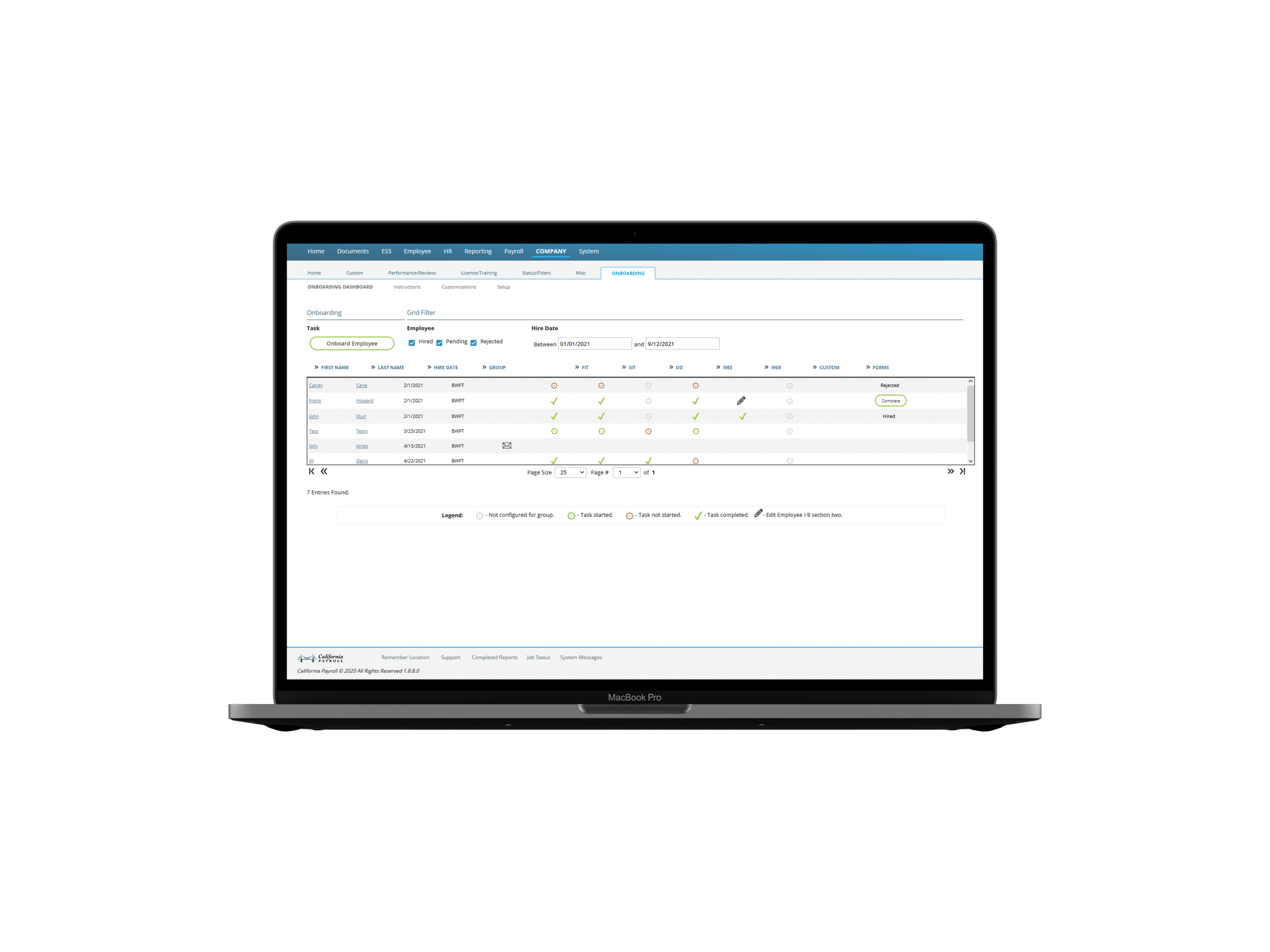

2. Set Up and Implementation.

California Payroll sets up and tailors a customized system to your company’s needs and includes individual training for your team.

3. Determine your company’s unique payroll, wage and hour needs and budget.

We don’t require you to fit your wage and hour needs in the same box. Your company is unique to us and we work with you to determine which of our products and services will best fit your team and your budget.